DTI Requirements for a Conventional Mortgage

When applying for a conventional mortgage, your debt-to-income ratio for a conventional loan approval may be one of the most important factors lenders evaluate. This financial measure helps determine your borrowing capacity and plays a central role in the underwriting process.

When applying for a conventional mortgage, your debt-to-income ratio for a conventional loan approval may be one of the most important factors lenders evaluate. This financial measure helps determine your borrowing capacity and plays a central role in the underwriting process.

Try our debt to income calculator

Understanding how conventional loan ratios work can improve your chances of loan approval and help you secure better interest rates. For a complete understanding of all qualification factors, review our comprehensive conventional loan requirements guide.

What is a DTI?

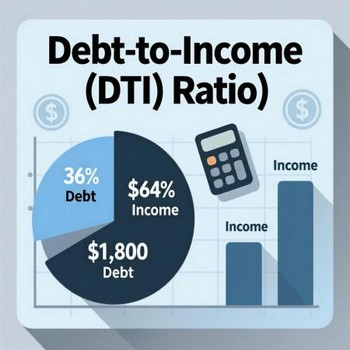

Your DTI for a conventional loan represents the percentage of your monthly gross income that goes toward paying debts, such as rent or mortgage. Lenders use this ratio to assess your credit standing and financial soundness.

The calculation includes all your recurring monthly debt obligations divided by your total monthly income before taxes to determine your debt-to-income calculator results.

There are two types of DTI ratio for conventional loan calculations that lenders examine. The conventional loan front-end ratio focuses specifically on housing expenses, including your mortgage payment, property taxes, insurance, and homeowners' association fees.

The back-end ratio for a conventional loan includes all monthly debt payments, such as credit card, student loan, auto loan, and personal loan payments.

Most lenders prefer a back-end ratio of 36% or lower for conventional loans, though some may accept higher percentages with compensating factors to accommodate a higher DTI. The front-end ratio typically should not exceed 28% of your monthly gross income.

How Lenders Calculate Your DTI

To calculate your conventional debt to income ratio, lenders add up all your monthly debt obligations. This includes your future monthly mortgage payment, credit card payments, car loan installments, student loan payments, and any other recurring debt.

They then divide this total by your gross monthly income.

For example, if your monthly debt payment totals $2,000 and your gross income is $6,000, your ratio equals 33.3%. This calculation helps lenders determine whether you can handle additional debt responsibly.

When you calculate your DTI before applying, include only the minimum credit card payment, not the full balance.

Lenders focus on the actual monthly payment requirements, not the total debt amount, when assessing your credit utilization assessment. This distinction can greatly affect your ratio calculation.

DTI Requirements for Conventional Mortgages

Conventional loan DTI limits typically require stricter standards compared to government-backed programs. Most lenders prefer a back-end ratio below 36%, though some may approve ratios up to 45% with strong compensating factors in the context of your maximum DTI for a conventional loan.

Your credit score, down payment amount, and cash reserves can influence how lenders evaluate your ratio.

Borrowers with excellent credit score requirements and substantial down payments may qualify with higher ratios than those with marginal credit profiles. The type of loan you choose can also affect DTI limits for conventional loan requirements.

Jumbo loans often have stricter ratio limits, while some conventional products offer more flexibility for qualified borrowers with a higher DTI. Understanding whether a conventional mortgage is better than an FHA loan can help you choose the right program for your DTI profile.

Key DTI Guidelines for Conventional Loans:

- Maximum back-end ratio usually ranges from 36% to 45%

- Front-end ratio should generally stay below 28%

- Higher ratios may require compensating factors

- Strong credit scores can offset slightly elevated ratios

- Larger down payments provide more DTI flexibility

How Your Ratio Affects Loan Approval

Lenders view your DTI for a conventional loan as a predictor of your ability to manage monthly mortgage payments. A lower ratio denotes better financial condition and reduces the lender's risk exposure.

This improved risk profile can lead to better loan terms and mortgage interest rates.

When your ratio exceeds standard guidelines, lenders may require supplementary documentation or compensating factors. These might include higher credit scores, larger down payments, or substantial cash reserves.

Some lenders may decline applications that exceed their maximum DTI for conventional loan thresholds.

Your ratio also impacts your loan qualification for different conventional mortgage products. Portfolio lenders may offer more flexibility than lenders that sell loans to government-sponsored enterprises, which have stricter ratio requirements.

Ways to Lower Your DTI Ratio

Improving this metric can expand your mortgage options and possibly secure better terms. The most effective approach is to either reduce monthly debt obligations or increase your income.

Paying down credit card debt provides immediate improvement in the ratio because it reduces the monthly payment requirement.

Focus on cards with the highest minimum payments first to maximize the impact on your ratio calculation. Think about consolidating high-rate debt into lower-payment options.

A personal loan with a lower monthly payment can improve your ratio while lowering overall interest costs.

However, avoid taking on new debt during the mortgage application process. Increasing your income through salary negotiations, additional work hours, or side employment can also improve your ratio.

Lenders typically require a two-year employment history for income consideration, so new income sources may not immediately help your application for what is the maximum DTI for a conventional loan.

Effective DTI Reduction Strategies:

- Pay down credit card balances to reduce monthly minimums

- Avoid taking on new debt before applying

- Consider debt consolidation for lower payments

- Increase income through career advancement or additional work

- Pay off smaller debts completely to eliminate monthly payments

Student loan payment calculator results may significantly affect your ratio, especially for recent graduates. Income-driven repayment plans may lower your monthly obligations and improve your debt-to-income ratio for a conventional loan.

Contact your loan servicer to consider available options for paying down debt.

Auto loan refinancing might reduce your car payment and lower your overall ratio. Shop around for better rates, especially if your credit score has improved since applying for a mortgage.

The amount of debt you carry relative to your income directly influences your mortgage qualification.

Lenders may suggest waiting to apply until you are able to achieve a more favorable ratio through debt reduction or income increases using an income qualification tool.

Understanding Fannie Mae DTI Standards

The Fannie Mae debt-to-income ratio guidelines set the foundation for many conventional loan programs. Conforming loan guidelines generally include DTI ratios of: 36% for the back-end ratio as a baseline standard.

However, Fannie Mae allows max DTI for conventional loan approval up to 45% with strong compensating factors.

Understanding what is the DTI for a conventional loan under Fannie Mae standards helps borrowers prepare realistic expectations. The conventional mortgage DTI limits consider your entire financial profile, not just the ratio alone.

Fannie Mae uses automated underwriting systems to evaluate applications.

These systems examine multiple factors including credit history, assets, and employment stability alongside your conventional loan income to debt ratio. Strong performance in other areas can offset a higher ratio.

Borrowers wondering what is the maximum debt to income ratio for a conventional mortgage should know that 50% represents the absolute ceiling in rare cases with exceptional compensating factors.

The max front-end DTI for a conventional loan typically remains around 28%, even though this can vary based on the total debt picture. Qualifying ratios for conventional loans balance both front-end and back-end calculations to assess overall affordability.

Your DTI limit for conventional loan approval depends on multiple variables working together.

Optimizing Your DTI for Better Loan Terms

Understanding your conventional DTI position before applying gives you time to make strategic improvements. Review your complete DTI guidelines to identify points for improvement.

Many borrowers benefit from using calculation tools to model different scenarios.

Consider how paying off specific debts would impact your overall ratio. Sometimes eliminating one or two smaller debts can make a notable difference in your conventional loan ratios profile.

Focus on debts with the highest monthly payments relative to their balances for maximum impact.

Your down payment planning also influences how lenders view your ratio. A larger down payment demonstrates financial strength and can offset a slightly higher DTI.

Some borrowers choose to delay their home purchase to improve their ratio position.

This waiting period permits time to pay down debt or increase income, resulting in better loan terms and potentially significant interest savings throughout the life of the mortgage. The conventional mortgage debt-to-income ratio you present at application directly affects your interest rate.

Lower ratios often qualify for better pricing and reduced fees.

Common DTI Mistakes to Avoid

Many applicants underestimate their actual monthly debt obligations when calculating their ratio. Include all recurring payments, even those you plan to pay off soon, unless you can document their elimination before closing.

Lenders verify your debts through credit reports and other documentation.

Opening new credit accounts during the mortgage process can damage your application. Each new account adds to your monthly obligations and may trigger additional underwriting review.

Wait until after closing to make major financial changes or take on new debt.

Some borrowers forget to account for the full housing payment when calculating their front-end ratio. Remember to include property taxes, homeowners insurance, private mortgage insurance, and HOA fees in your calculations.

These costs greatly affect your monthly housing expense.

Depending exclusively on online calculators without understanding how lenders actually calculate ratios can lead to surprises during underwriting. Work with a qualified loan officer who can provide accurate calculations according to your specific situation.

They can identify possible issues before you apply and recommend solutions.

Conclusion

Your DTI acts as a fundamental measure of your financial capacity and mortgage readiness. Understanding how lenders evaluate this metric enables you to make informed decisions about when to purchase your home and which financing options to pursue.

Taking steps to optimize your ratio before applying can grant access to better loan terms and smoother approval processes.

When preparing for a conventional mortgage application, focus on achieving a ratio that demonstrates strong financial management. This preparation shows lenders your devotion to responsible borrowing and increases your chances of gaining favorable loan terms for your home purchase.

Frequently Asked Questions

What is the maximum DTI allowed for a conventional loan?

The maximum DTI for conventional loans usually ranges from 45% to 50%, though most lenders prefer ratios below 43%. Fannie Mae and Freddie Mac set these standards, but individual lenders may have stricter requirements. Borrowers with ratios above 45% usually need strong compensating factors such as excellent credit scores, large down payments, or substantial cash reserves to qualify for approval.

How is the front-end ratio different from the back-end ratio?

The front-end ratio only includes housing-related expenses such as mortgage principal, interest, taxes, insurance, and HOA fees divided by gross monthly income. The back-end ratio includes all monthly debt obligations, including housing costs, credit cards, auto loans, student loans, and other recurring debts. Lenders evaluate both ratios, with front-end ratios typically capped around 28% and back-end ratios around 36% to 45% for conventional loans.

Can I qualify for a conventional loan with a 50% DTI?

Qualifying with a 50% DTI is possible but challenging and requires exceptional compensating factors. You would need an excellent credit score, typically above 740, a substantial down payment of at least 20%, and significant cash reserves covering several months of payments. Most lenders reserve these higher ratios for their strongest borrowers, and automated underwriting systems must approve the higher ratio based on your overall financial profile and risk assessment.

Does paying off debt before closing help my DTI?

Yes, paying off debt before closing can improve your DTI and loan approval chances. However, you must provide documentation proving the debt has been paid in full, and lenders will verify this information before final approval. Focus on paying off debts with high monthly payments relative to their balances for maximum impact. Avoid paying off debts through depleting your cash reserves, as lenders also require adequate funds for closing costs and reserves.

How do lenders count student loan payments in DTI calculations?

Lenders typically use either the actual monthly payment on your credit report, 1% of the outstanding balance, or the payment shown on an income-driven repayment plan documentation. If your loans are in deferment or forbearance, lenders may still include a calculated payment in your DTI. Providing documentation of your actual payment amount, especially if you have an income-driven repayment plan with a lower payment, can help reduce your calculated DTI ratio.

Connect With Us

Please share – it really helps