Conventional Loan Credit Score Requirements

Your credit score is a big deal when you're trying to buy a home. When you apply for a conventional loan, lenders will dig into your credit history to see how likely you are to pay them back.

Your credit score is a big deal when you're trying to buy a home. When you apply for a conventional loan, lenders will dig into your credit history to see how likely you are to pay them back.

Unlike government-backed options like FHA or VA loans, conventional mortgages come from private lenders. These lenders follow rules set by Fannie Mae and Freddie Mac, which help preserve consistency across the country.

What’s the Minimum Credit Score for a Conventional Loan?

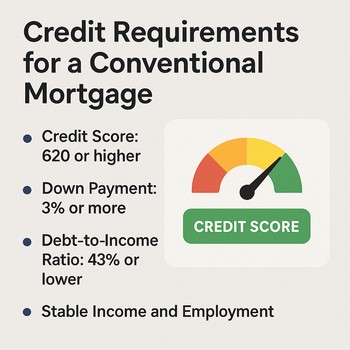

Most lenders want to see a minimum credit score for conventional loans of at least 620. Think of 620 as the entry ticket. It might get you in the door, but a higher score gets you a much better seat.

The difference between a 620 and a 720 score is huge. We're discussing possibly lower monthly payments and saving tens of thousands of dollars in interest over a 30-year loan.

That three-digit number tells lenders about your payment history, your debts, and how long you've managed credit. Borrowers with strong credit usually get approved faster and with fewer strings attached.

Beyond Your Score: The Full Qualification Picture

Meeting the credit requirement for conventional loan approval is just one piece of the puzzle. Lenders also look at several other key factors before saying yes.

They'll examine your debt-to-income ratio (DTI), your job history, your savings, and other assets. Each part helps build a complete picture of your economic status.

Most lenders prefer a DTI below 43%. But there's some wiggle room if you have strong compensating factors, such as a large down payment or excellent credit. In some cases, they might go up to 50%.

Wait, what about my job and income?

You'll need to show a steady income, usually with at least two years of consistent employment in the same field. If you're self-employed, expect to provide two years of tax returns and profit-and-loss statements.

Don't forget about closing costs (typically 2-5% of the home's price). The minimum down payment for first-time buyers can be as low as 3%. But remember, putting down less than 20% means you'll pay private mortgage insurance (PMI) until you build more equity.

Key Credit Factors That Make or Break Your Qualification

Your payment history is the most important thing in your credit score. Late payments, collections, or bankruptcies can hurt your profile for years.

How much debt you're carrying right now matters too. High balances compared to your credit limits look risky to lenders and can hurt your DTI calculation.

Here are a few other things lenders notice:

- Length of credit history: A longer history gives lenders more data on your financial habits.

- Credit mix: Having both revolving accounts (credit cards) and installment loans (auto loans) shows you can handle different types of debt.

- New credit applications: Too many recent applications can temporarily lower your score and raise red flags. Avoid opening new cards or taking out car loans for at least six months before applying for a mortgage.

Conforming Loan Limits and the Secondary Market

A conforming conventional loan has to meet specific rules set by Fannie Mae and Freddie Mac. These two companies buy mortgages from lenders, which gives lenders more cash to make new loans to people like you.

For 2026, there's a baseline limit for most single-family homes. But in high-cost areas like Alaska, Hawaii, or expensive metro regions, the limits can be much higher. If your loan fits within these limits, you often get better interest rates because lenders see it as lower risk.

Types of Conventional Loans: Fixed vs. Adjustable Rate

Understanding your options helps you pick the right loan for your situation. A fixed-rate mortgage keeps your interest rate the same for the entire loan term (usually 15 or 30 years). This makes budgeting super predictable.

An adjustable-rate mortgage (ARM) starts with a lower rate that stays the same for a set period (like 3, 5, or 7 years) before it can change. ARMs can be great if you plan to sell or refinance within a few years.

What About Government-Backed Loans?

Government-backed loans work differently. For example, FHA loans accept credit scores as low as 500 with 10% down, or 580 with just 3.5% down. That's great for first-time buyers.

But here's the trade-off: most FHA loans require mortgage insurance for the entire loan term, which adds up. VA loans offer incredible benefits (no down payment, no monthly insurance) for eligible military members. USDA loans also offer zero-down financing for rural areas.

One big advantage of conventional loans? You can cancel PMI once you reach 20% equity. That can save you a lot compared to federally backed loans, which require insurance for the life of the loan.

How to Build and Improve Your Credit Profile

If your score is below that 620 threshold, don't panic. You can take steps to improve it before you apply. Start by getting free copies of your credit reports from all three major bureaus and checking for errors.

Dispute any mistakes you find. Then, pay every single bill on time. Payment history makes up 35% of your FICO score, so this is huge.

Quick strategies to boost your score:

Pay down your credit card balances. Experts say to keep your utilization below 30%, but your score really jumps when you get below 10%. Avoid opening any new credit accounts in the months leading up to your mortgage application.

Raising your score pays off. A borrower who goes from a 620 to a 680 could save thousands in interest. Even a 0.25% rate reduction saves tens of thousands over the life of the loan.

Preparing Your Application for Success

Get your documents together early. You'll need pay stubs, W-2 forms, tax returns (usually for the last two years), and bank statements. Self-employed? Add business returns and profit-and-loss statements.

Your lender will pull your credit, which creates a hard inquiry. This might drop your score by a few points, but it's temporary. And if you shop for rates within a 14-45-day window, multiple inquiries count as a single pull.

The whole process takes patience, but good preparation pays off. From meeting the conventional loan credit score requirements to managing your DTI, each detail is important. Ask questions if you're confused. A good loan officer will walk you through every step.

Achieving Homeownership Through Smart Planning

Proper preparation turns the dream of homeownership into reality. Take time to improve your credit, save for a down payment, and organize your paperwork. The effort you invest now will save you money for years to come.

Your success depends on understanding the conventional loan credit score requirements, preparing carefully, and working with pros who have your best interests in mind. You've got this.

Frequently Asked Questions

Can I qualify with a 580 credit score?

Most conventional lenders will say no below 620. That's the industry standard. However, FHA loans accept scores as low as 580 with a 3.5% down payment. Consider government-backed programs if your score is below 620 while you work to improve it.

How much should I save for closing?

Closing costs typically run 2-5% of the purchase price, plus your down payment. First-time buyers can put down as little as 3% through special programs. Lenders also want to see that you have savings left over after closing for emergencies.

Does shopping for mortgage rates hurt my credit?

Multiple mortgage inquiries within a 14-45 day window count as just one pull for scoring purposes. This protects your score while you compare lenders. Each hard inquiry might lower your score by fewer than 5 points, but the impact fades quickly.

What documents do self-employed borrowers require?

Self-employed applicants need two years of personal and business tax returns with all schedules. Lenders also require current profit-and-loss statements and sometimes a letter from your CPA verifying income and business stability.

How much can I save by improving my credit score?

A lot. A borrower who raises their score from 620 to 680 could save thousands in interest charges over a 30-year term. Even a 0.25% reduction in your interest rate saves tens of thousands of dollars over the life of the loan. The higher your score, the lower your rate and the more you save each month.

Connect With Us

Please share – it really helps