Conventional Cash-Out Limits

Let’s talk about conventional loans. They're a big category. Basically, any mortgage not backed by the government (like FHA, VA, or USDA) falls under this umbrella.

Let’s talk about conventional loans. They're a big category. Basically, any mortgage not backed by the government (like FHA, VA, or USDA) falls under this umbrella.

Private lenders issue these loans. They follow their own guidelines. But there's a special sub-category you need to know about: conforming loans.

A conforming loan sits inside the conventional world. It has one extra rule: it must meet the purchase standards set by Fannie Mae and Freddie Mac. The most important standard? Loan size.

Every year, the Federal Housing Finance Agency (FHFA) sets a max cash-out for a conventional loan limit (well, for conforming loans, which are the most common conventional type). This number changes. And it matters a lot for your wallet.

When your mortgage falls under that threshold and meets basic credit rules, it becomes "conforming." Lenders love these. They're easy to sell. That means better rates and more flexible approvals for you.

Go over the limit, and you enter jumbo loan territory. Jumbos are still conventional, but Fannie and Freddie won't touch them. That usually means stricter underwriting and tougher qualification standards.

What Changed in the 2026 Loan Limits

For 2026, the FHFA raised conforming loan limits again. Why? Home prices kept climbing. This annual adjustment isn't random.

It's designed to stop housing inflation from pushing ordinary buyers into jumbo territory. Without these updates, rising home values would force more people into harsher lending rules. That's not fair, and the FHFA knows it.

With the new 2026 limits, more properties qualify for conforming financing. This improves affordability. It also expands borrowing options, whether you're looking at an entry-level condo or a mid-priced family home.

Baseline vs. High-Cost Area Limits

Most counties fall under a national baseline conforming limit. But housing markets aren't uniform. The FHFA applies higher limits in expensive regions where home prices consistently beat national averages.

These high-cost area limits keep financing accessible. If you live in a pricey metro area, you can still get a conforming loan even when homes cost way more than the national norm.

Multi-unit properties (duplexes, triplexes, fourplexes) also get higher limits. They represent larger loan exposure and income-producing potential. So the rules adjust for that too.

Why the 2026 Increase Matters for Buyers

More Homes Now Qualify for Conventional Pricing

One immediate effect of higher limits is expanded access to conventional loan pricing. Conforming loans usually have lower rates than jumbo loans. That's because lenders can sell them to Fannie and Freddie, reducing risk.

They also deliver broader approval flexibility. Think lower-down-payment options for qualified borrowers. Think more-forgiving credit profiles than jumbo standards.

As home prices rise, this shift is huge. Properties that once needed jumbo financing may now fall within conforming limits. That changes your monthly payment expectations and your odds of approval.

Refinancing Opportunities Created by Higher Limits

Rising limits also help current homeowners. Has your property appreciated? Your existing loan might now fit inside conforming guidelines.

That opens the door to refinancing from a jumbo mortgage to a conventional conforming loan. This switch can lower your interest rate and simplify the underwriting process. It might even eliminate those strict reserve conditions that jumbo loans love to demand.

In some cases, you'll have access to streamlined refinance programs. Less paperwork, lower cost barriers. Always ask your lender.

Conforming vs. Jumbo Loans: Key Practical Differences

Once a loan exceeds conforming limits, you're in jumbo territory. The differences aren't cosmetic. They affect qualification, cost, and flexibility in real ways.

Credit Score Expectations

Conforming loans can be accessible to borrowers with moderate credit profiles. Jumbo loans typically require stronger credit, often starting around 700 or higher. Best pricing goes to high-tier borrowers.

Down Payment Requirements

Conforming mortgages often allow lower down payments. Sometimes as low as 3% for qualified buyers. Jumbo loans usually require much more upfront equity - typically 10% to 20% or higher, depending on loan size.

Debt-to-Income Constraints

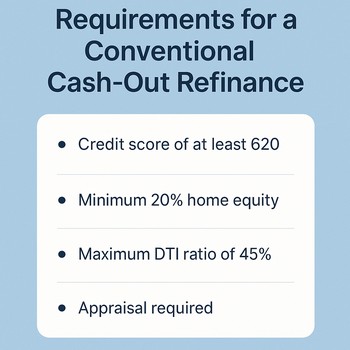

Conforming loans may allow higher debt-to-income ratios in certain scenarios. You might approach 45%–50% with compensating factors. Jumbo loans are more restrictive, often capping ratios near 40%–43%.

Cash Reserve Requirements

Jumbo lenders frequently demand extra cash reserves after closing. That could be several months of payments or more. Conforming loans are less demanding here, making them easier to qualify for if your liquidity is limited.

Interest Rate Dynamics

Jumbo loans are often associated with higher rates, but that's not guaranteed. For highly qualified borrowers, jumbo rates can sometimes match or even beat conforming rates. Market conditions and lender competition play big roles.

Understanding Conventional Loan Cash-Out Limits

Now, let's get specific about pulling equity out. A cash-out refinance lets you replace your existing mortgage with a larger one. You take the difference as cash. But there are strict caps.

The cash out refinance ltv limits on a conventional loan are different from a rate-and-term refi. LTV means loan-to-value. It's how much you borrow compared to your home's worth.

For a conventional cash-out refinance, the conventional max cash out ltv is typically 80%. That means you must leave 20% equity in your home. You cannot borrow more than 80% of your home's current value.

This is a key limit. The maximum loan to value on a conventional cash out refinance is firmly set at 80% for most primary residences. There are rare exceptions for certain property types or portfolio loans, but the standard rule is 80%.

So what are the conventional loan cash out limits in dollar terms? That depends on your home's value and the conforming loan limit in your county. You cannot exceed either the 80% LTV cap or the maximum loan amount for your area.

For example, if your home is worth $500,000, the max cash-out loan amount is $400,000 (80% LTV). But if your county's conforming limit is $450,000, you're fine. If the limit is $350,000? You'd be restricted to that lower number.

Knowing these limits helps you plan. Before you apply, know your home's current value and your county's conforming cap. Then calculate 80% of that value. The smaller number is your likely ceiling.

Why Conforming Loan Limits Should Guide Your Strategy

Conforming loan limits aren't simply technical thresholds. They directly shape what mortgage you qualify for and how much it will cost over time.

A small change in the annual limit can decide whether you get lower-cost conventional financing or shift into jumbo underwriting with stricter conditions. That affects approval odds, long-term affordability, monthly payments, and total borrowing cost.

For cash-out refinances, these limits work together with the 80% LTV rule. Always check both numbers. And remember: investment properties and second homes often have tighter rules than primary residences.

Frequently Asked Questions

How do I find my county's conforming loan limit?

The FHFA publishes updated loan limits annually by county. You can find them on the FHFA website. Or just ask any lender - they can do an instant lookup based on your property's ZIP code.

Do conforming limits apply to investment properties?

Yes, they do. But investment properties and second homes typically require higher down payments. Qualification standards are also stricter than for primary residences. Expect to put more money down and show stronger reserves.

Is PMI required on conforming loans?

Yes, if your down payment is under 20%. PMI (private mortgage insurance) protects the lender. The good news? You can usually remove PMI once you reach sufficient equity, typically 20-22% of the original home value.

Can gift funds be used for down payments on a conventional cash-out refi?

For a purchase, yes, gift funds are frequently allowed. For a cash-out refinance, you're not making a down payment - you're pulling equity out. But gift funds generally cannot be used to meet reserve requirements. Check with your specific lender.

How do I know how much I can actually borrow?

Your borrowing limit depends on your income, existing debts, credit score, and local conforming limits. For a cash-out refinance, your max cash out for a conventional loan is the lowest of: 80% of your home's value, your county's conforming limit, or what you can afford based on your debt-to-income ratio. A lender preapproval is the most accurate way to get your real number.

Final Summary

The 2026 increase in conforming loan limits expands access to conventional mortgage financing for many buyers and homeowners. In plain English, more people may qualify for lower-rate, more flexible loans rather than being pushed into stricter jumbo loan requirements.

For cash-out refinances, remember the golden rule: you're typically capped at 80% LTV. And you cannot exceed your county's conforming limit. Understanding where your home's value fits within these limits will directly affect your financing options - and the overall cost of your mortgage.

So check your numbers. Talk to a lender. And know that those annual limit adjustments aren't just bureaucracy - they might just save you a bundle.

Connect With Us

Please share – it really helps